On-chain credit markets may define crypto’s next stage in 2026 by linking two areas that once operated separately: open financial systems and real-world lending. Not long ago, borrowing in DeFi usually meant pledging extra cryptocurrency just to borrow a smaller amount.

These loans stayed mostly inside crypto-native circles. Users handed over more value than they received, often using volatile tokens as collateral. Risk control happened automatically, triggered when prices dropped too far.

Back then, the system worked, but only within tight limits. It served traders, yield chasers, and crypto firms better than regular companies or people needing loans. In 2026, the conversation sounds different. Liquidity volume is no longer the only concern. Now comes a tougher question: can blockchains actually support how credit takes shape?

This changes how we see lending. On-chain credit markets are not merely a new type of loan. Instead, they create links between crypto capital, tokenized real-world assets, stablecoins, private debt, and traditional banking through quieter connections. That bridge matters.

Contents

- 1.On-Chain Credit Markets Explained Simply

- 2.Why 2026 Stands Apart

- 3.From Overcollateralized DeFi to Real Borrowing

- 4.Institutions Notice the Shift

- 5.Tokenized Real-World Assets and Their Function

- 6.Stablecoins Handle Transactions Behind the Scenes

- 7.The Appeal of On-Chain Credit

- 8.The Risks Are Real

- 9.Why This Trend Might Continue

- 10.What to Watch in 2026

- 11.Credit Stretches Crypto’s Limits

- 12.FAQ

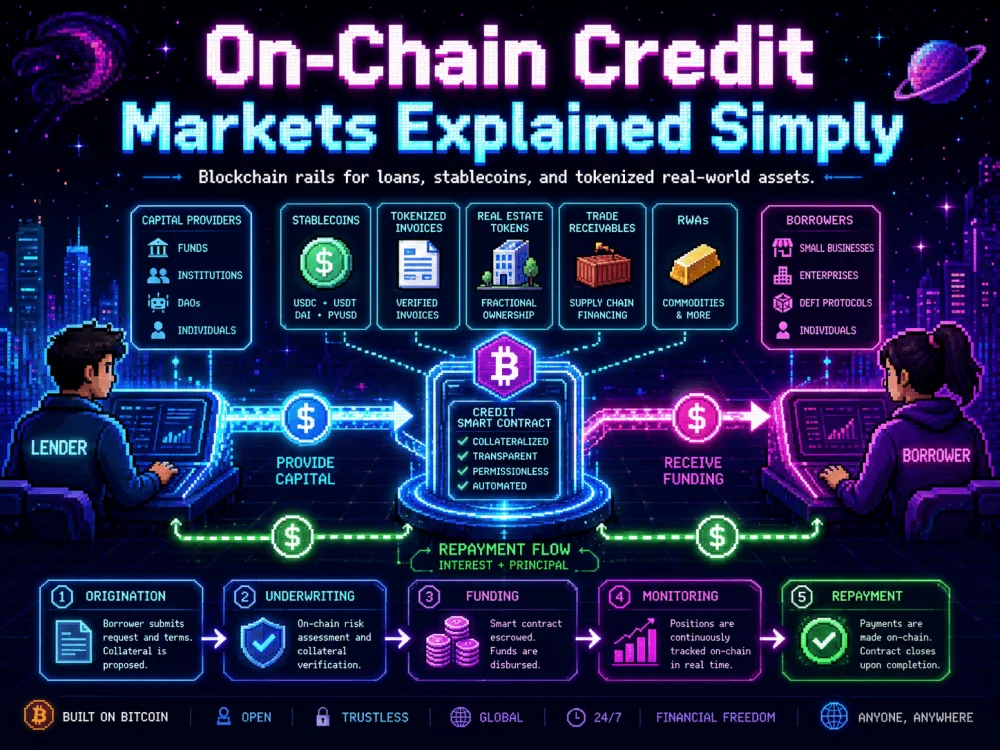

On-Chain Credit Markets Explained Simply

Loans built directly into blockchain systems can be started, funded, watched, or settled using that technology. Stablecoin borrowing backed by digital assets can stay fully within cryptocurrency markets. In other cases, real-world items like company invoices may back these debts. Trade finance between businesses can be tied to them too. Private lending pools may connect here. Corporate debt appears in some versions of this system.

One key change is transparency. The lending system becomes easier to track and more programmable. Loan terms, collateral movement, repayment schedules, and investor claims can appear on-chain. This is not a fix for default risk. Yet it helps with tracking, checking, and streamlining parts of financial work.

Most traditional lending systems feel fragmented. Investors may get their first real look at loan performance only when updates finally arrive. Payments can drag on before they clear. Middlemen decide who gets access. Smaller participants may never reach global funding pools. Newer lending setups running on blockchains replace paper-like records with digital tokens, shift payouts to stablecoins, and build deals inside code that runs automatically.

Faster money flow draws people in. Clearer proof of ownership matters too. Access to income-generating loans could reach more participants. Speed plus transparency sticks. Clean ownership trails make trust easier. New paths to earning interest open up for some investors.

Related: The Next Solana? Emerging Blockchain Projects Gaining Massive Attention

Why 2026 Stands Apart

Credit has always been larger than speculative trading. Crypto spent years proving that digital value could move across borders. Yet building real trust in code-based financial agreements remained the harder challenge.

By 2026, the issue feels less theoretical. Multiple shifts are happening together.

First, stablecoins have moved beyond being seen only as trading assets. They are now viewed as payment and settlement tools. Because of this shift, dollar-based loans can be issued and repaid at any time, day or night, without old banking schedules. As a result, on-chain credit markets finally have a practical method for handling money transfers smoothly.

Second, tokenized real-world assets have moved past early testing. Treasury products, fund tokens, and private credit pools now appear more often on blockchains where the legal and operational setup makes sense. Institutions seem ready to place familiar financial tools on-chain when the conditions line up.

Third, private credit shapes much of today’s financial world. With banks still careful about who they lend to, businesses keep looking elsewhere for capital. Instead of waiting on traditional routes, many lean into non-bank options. Crypto systems are trying to step into this opening by offering clearer structures for pooled lending. These networks may open doors usually kept shut, reshaping how groups pool resources across borders.

What stands out in 2026 is not just another spike in DeFi lending. Instead, attention has shifted toward actual function: can blockchains manage credit tasks reliably? Past loops of inflated returns fade here. The focus lands elsewhere: performance under real demands. Not hype, but practical testing.

Related: Why Crypto Regulation Became a Global Power Issue in 2026

From Overcollateralized DeFi to Real Borrowing

Lending in old-school DeFi works fine, just not for everything. When someone has to lock up $150 or even $200 to borrow $100, it helps with leverage, liquidity management, or tax planning. Yet a company looking to grow will not get far with that kind of setup.

Most people and companies needing loans rarely own piles of ready-to-use collateral. Getting access to funds often ties back to earnings, property, pending payments, track record, lender reviews, or future income streams. Lenders look at these factors closely. Simple asset counting does not cover it. Real lending means judging repayment ability, not just totaling up sellable items.

This is where on-chain credit markets are shifting slowly. They are no longer only about fixed collateral rules. Mixed approaches are appearing. Crypto stays as backing in certain cases. Tokenized physical assets step in elsewhere. Off-chain assessments feed data into blockchain systems for some setups.

Most of the time, mixing old rules with new finance gets messy. Legal papers show up, identities matter, collateral needs checking, and when things go wrong, there has to be a recovery process. Yet exactly because of those steps, bigger opportunities open up. Lending money is not just about cutting losses automatically. Figuring out whether someone will pay back takes real judgment.

Institutions Notice the Shift

Big money managers like credit deals because they can bring steady returns, diversify portfolios, and connect investment to actual business activity. Digital assets often paid out through speculation, reward tokens, or heavily stacked leverage. Repayment-driven yield stands apart because it comes from borrower payments, not only market mood swings.

In a maturing market, that difference matters. When returns seem too high without explanation, investors ask harder questions. People start asking what backs the numbers. Real names help. So does knowing who owes what, when payments are due, and what happens if promises break. Proof sits better than guesses. A payment timeline, collateral, and clear details speak louder than vague claims.

Read more: Hedera (HBAR) Price Prediction 2026: Institutional Adoption, Valuation Model & Long-Term Forecast

Tokenized credit attracts asset managers because it can reduce back-office friction. Settlements move quicker when paperwork turns into code. Fund shares become simpler to follow across systems. Payouts can happen without manual checks. Crypto-savvy buyers get a path into lending strategies once locked behind membership walls. Private debt used to mean gatekeepers and long forms. Now blockchain systems are opening some doors quietly.

Still, big players will not jump into any platform offering loans. Legal setup matters. So does reporting quality. Control over assets plays a role too. Past defaults leave marks. Regulators shape decisions. Poorly built systems eventually lose favor. That is simply how credit works.

Tokenized Real-World Assets and Their Function

Tokenized real-world assets are pushing on-chain credit markets forward. Lending relies on collateral, income streams, and legal rights. Tokenization gives those rights a digital wrapper, letting them move across blockchain networks. Movement gets faster when ownership becomes data that lives online. Settlements can clear more efficiently once value becomes programmable.

Sometimes this involves business lending, real estate debt, trade finance, unpaid bills, income-linked funding, or structured debt products. Though the actual asset may sit outside the blockchain, ownership proof or investor claims can live on-chain.

One big advantage is clearer insight for investors watching how pools perform. Issuers may reach more funding sources. Faster settlement appears as another benefit. Automation can handle payouts without constant oversight. Over time, secondary market trading might improve, though that promise often gets stretched too far.

The caution is simple. Turning a shaky loan into tokens will not fix its flaws. Just because debt runs on blockchain does not mean the borrower will pay. What really shapes trust in digital lending is how loans are checked, how clear records stay, and whether payments can be collected. Strong structure beats clever coding every time.

Stablecoins Handle Transactions Behind the Scenes

Hidden beneath this shift, stablecoins do much of the quiet work. A steady unit of account matters in nearly every lending system. When debt values jump around with Bitcoin, borrowers lose sleep. Repaying loans gets harder if the money owed changes sharply each day.

When debt, returns, or payouts are tied to dollar-pegged tokens, things settle down. These digital assets keep value relatively stable while moving across blockchains. Suddenly, online lending feels less strange to people borrowing locally or investing from abroad.

Cross-border loans feel this shift first. Old-style payments often drag on, cost too much, or shut people out without warning. Moving money through stablecoins can speed things up, make transaction trails more transparent, and reduce settlement delays.

Yet stability brings new dependencies. The strength of the backing matters, as does the issuer. Rules set by authorities play a role too, along with ties to traditional banks. When payments run on stablecoins, every weakness in those coins shows up later in lending risks. Dependability becomes concrete exposure.

Related: USDT vs EU Regulation: Why Tether Is Facing Legal and Compliance Challenges in Europe

The Appeal of On-Chain Credit

On-chain credit markets shine brightest when seen through the right lens. Removing all middlemen is not the real story. That idea oversimplifies things. Actual lending systems usually rely on originators, underwriters, servicers, auditors, and legal agents.

The stronger argument is that blockchain systems can streamline certain steps. Efficiency gains may come from how these tools handle data, payments, claims, and reporting.

Key advantages include:

- Faster settlement for lending and repayment flows

- More transparent loan pool reporting

- Programmable interest distributions

- Tokenized investor claims

- Broader access to private credit strategies

- Potential secondary markets for credit exposure

- Better integration with DeFi liquidity

Real gains come from usefulness, not fantasy. Overnight transformation of credit systems is not what drives adoption. What matters is whether blockchain infrastructure can support certain functions better than current methods in speed, cost, or openness. Progress shows up where it works best, not everywhere at once.

The Risks Are Real

The trend looks promising, but when loans move to blockchain, risk comes with them. A digital ledger will not stop someone from skipping payments. The value of collateral might be wrong. Debt issuers could fail. Courts may not back a claim as expected. Reports may leave out key facts or twist them.

Code problems can still cause trouble. Even solid lending rules will not help if the software has flaws. On the other side, perfect code means little when the loans are risky. Mistakes in either area put investor funds at stake.

Not every digital token moves easily. Even if a loan lives on-chain, that does not mean it can be sold fast. A rush to exit could leave sellers waiting. The real asset behind the token might lock money up for years. Digitizing the claim will not fix that gap.

Rules shape outcomes just as much as code does. Credit is not a loose category. The moment systems involve actual borrowers, yield-generating instruments, debt resembling bonds, or shared loan pools, regulators start paying attention. Those who build lasting positions here probably will not tack on rules after launch. They will weave them into the foundation from day one.

Why This Trend Might Continue

Some crypto fads flare up and vanish. Yet on-chain credit markets may last longer because they answer a deep demand: access to capital.

Money keeps companies running. Investors want returns on what they put in. Digital dollar owners need ways to make their holdings work. Asset managers search for faster ways to move value. Settlements often drag, slowing everything behind them. Blockchain protocols need income sources beyond price swings. Their survival depends less on hype now. Yield must come from actual use, not just trading.

Most talk fades fast. Real strength shows up later. When digital records help money flow better, even in one corner of finance, something sticks. Growth then has a path. Hype cracks under weight. This does not have to.

One step at a time seems more probable than wiping out banks overnight. Imagining everything replaced right away is just building castles in thin air. Real change creeps in sideways, not head-on. Lenders, fund managers, fintech firms, and crypto protocols may each use blockchain where it speeds things up: clearing records faster, sharing data more smoothly, and reaching investors more widely. Not revolution. More like old systems meeting new tools where the fit makes sense.

So the idea is not about dragging every single loan onto a blockchain. What matters is showing that real lending can happen there enough to prove these digital pathways work.

What to Watch in 2026

One way to tell whether on-chain credit markets will last is by tracking specific signs. A few metrics reveal more than headlines ever could. Staying power often shows up in slow shifts, not sudden jumps. Patterns emerge when activity holds steady over weeks or months. What looks trendy might actually be taking root beneath the surface.

Loan performance comes first. More money locked up will not matter much if repayments slip or data gets fuzzy. Borrower quality comes next. When stronger borrowers enter the market, it shows the system is moving past trial runs. Then comes institutional involvement. When serious capital steps in, it brings pressure for clearer reporting and tougher legal structures.

Secondary liquidity is another factor. When tokenized credit trades smoothly without fake volume, interest grows naturally. Integration with stablecoins and real-world asset systems matters too. Scaling up demands reliable settlement methods plus access to verified asset details.

Regulation wraps it up. Clearer rules might cool down certain experiments, yet strengthen those playing long-term. This balance could be healthy. Credit markets need trust; good luck lasting on feelings alone, no matter how hard crypto keeps trying.

Credit Stretches Crypto’s Limits

These days, on-chain credit markets are growing by turning digital money into tools for building value. Instead of only swaps and bets, crypto infrastructure can now support real loans through code-based systems. Smart contracts can handle payments while investors earn from private debt strategies. Stablecoins can move where returns rise across global pools. Behind it all, pieces fit together: digital receipts, market networks, and verifiable records.

Big rewards may sit ahead, but danger still stays close. Loud promises will not win. Solid foundations will. Trust comes from clear terms, open records, working safeguards, smooth payouts, and steady controls. Success depends on proof, not noise.

Crypto has already shown that assets can move on-chain. The next question is whether debt obligations can move there too. By 2026, that question is no longer theoretical. It is one of the biggest tests facing crypto markets today.

FAQ

What are on-chain credit markets?

On-chain credit markets are lending systems that use blockchains to start, fund, track, settle, or represent loans. They can include crypto-backed loans, tokenized private credit, invoice financing, real-world asset lending, and other credit products.

Why are on-chain credit markets trending in 2026?

They are trending because stablecoins, tokenized real-world assets, private credit demand, and DeFi infrastructure are converging. Together, they make blockchain-based lending more practical than it was in earlier cycles.

Are on-chain credit markets the same as DeFi lending?

Not exactly. Most DeFi lending needs more collateral than the loan value. On-chain credit markets can go further by connecting real borrowers, tokenized real-world assets, risk checks, and repayment cash flows.

What are the biggest risks?

The biggest risks include borrower default, weak underwriting, poor reporting, legal enforcement problems, smart-contract flaws, liquidity mismatches, and shifting regulation.

Could on-chain credit replace traditional lending?

Not soon. The more likely path involves integration instead of replacement. Settlement, transparency, distribution, and access could improve through blockchain rails, while human credit judgment still matters.