A new Bank of Canada study says DeFi lending can exist without banks in the middle, but the money and the pain are both highly concentrated.

Canada’s central bank, the Bank of Canada, has wrapped up a study on DeFi lending, zooming in on Aave V3 specifically, and found that decentralized crypto lending can work, though it’s not risk-free.

In a 32-page study titled “DeFi Lending: Returns, Leverage, and Liquidation Risk” and published Thursday, April 2, the Bank of Canada’s senior research analyst Jonathan Chiu and Furkan Danisman from the University of Toronto praised Aave for its design as the protocol provides services “continuously, transparently, and with minimal overhead, demonstrating the potential of protocol-based credit markets.”

Even so, the paper notes the system leans heavily on a handful of assets and user sentiment, which is where retail investor risk starts to show up.

Contents

Aave’s Crypto Earnings Are Mostly Stuck in a Few Tokens

The money side is pretty concentrated. Wrapped Ethereum (WETH), Tether (USDT▲$0.9995) and USD Coin (USDC▲$0.9998) make up nearly 83% of total earnings, and “a small subset of tokens accounts for most of the platform’s lending revenue,” the paper reads.

For retail traders, the bigger story though is leverage. The study praises recursive borrowing, where users borrow against crypto, then redeposit it to borrow even more, as a unique DeFi feature, noting that margin-style borrowing made up about 20% of borrowed volume but only 8% of transactions.

Wrapped Tokens Lead Liquidations on Aave

But that feature is also where liquidations hurt. Aave’s docs say positions can be liquidated when the health factor drops below 1, letting liquidators repay debt and grab collateral at a discount.

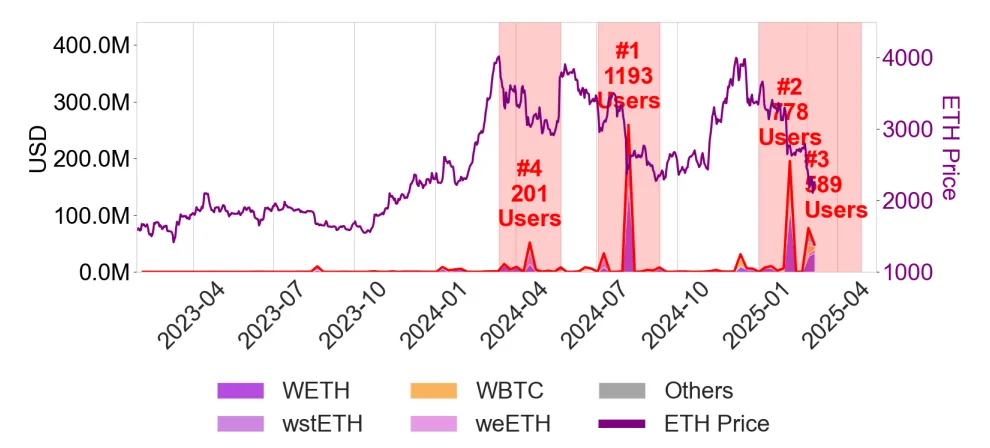

The Bank of Canada paper says only four tokens — WETH, wstETH, WBTC and weETH — account for 90% of liquidated value, with the largest wave topping $250 million. The paper also reads:

“Additionally, we observe that sharp price declines in ETH▼$1,575.91 are strongly associated with spikes in liquidation volume, underscoring the system’s sensitivity to major asset price movements.”

The study didn’t see clear signs that these liquidation waves move crypto prices long-term, though short-term pressure does show up in simple models. Overall, the paper concludes that DeFi lending works, but issues like idle funds, overcollateralization, and heavy leverage still make it risky for regular investors.