A Mt. Gox Bitcoin wallet moved 10,306 BTC▲$62,630.00 worth about $731 million, reviving focus on creditor repayments as BTC trades near weaker levels.

Crypto exchange Mt. Gox remains one of Bitcoin’s longest-running supply overhangs, even years after the Tokyo-based exchange collapsed and left creditors waiting for repayment.

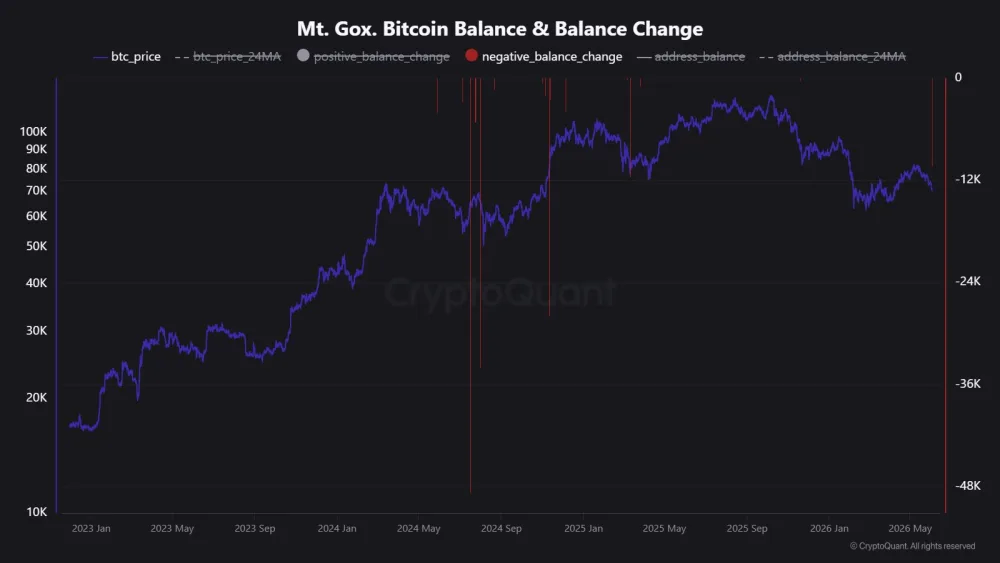

CryptoQuant, a blockchain analytics firm, said in a Tuesday post on X that a wallet linked to the defunct crypto exchange moved more than 10,000 BTC, resembling earlier transfers tied to creditor repayments and distribution preparation.

As CryptoQuant argued, previous such transfers “did not lead to immediate selling pressure,” even though Bitcoin is already under pressure. As Bitcoin Foundation reported earlier, BTC declined to $70,000, down 4% on the day, putting it close to the $69,000 area last seen in early April.

The latest move also came after Strategy, the largest publicly traded holder of Bitcoin, disclosed its first standalone BTC sale in years. The company sold 32 BTC between May 26 and May 31 to help fund dividends on STRC, its perpetual preferred stock known as Stretch.

Read also: Why Bitcoin Education is More Important Than Ever in 2026

Mt. Gox Repayment Risk Returns

Mt. Gox collapsed in 2014 after losing hundreds of thousands of BTC. The exchange remains one of the market’s longest-running supply overhangs.

Its trustee has been working through creditor repayments for years. The final repayment deadline has been pushed to Oct. 31, 2026.

Public wallet reports in March put Mt. Gox-linked holdings at about 34,504 BTC. But that figure should be treated as a rough tracker since coins can just move between trustee-controlled wallets without immediately going to creditors.

In 2024, Bitcoin also fell as much as about 4% around the Mt. Gox wallet moves, dropping to roughly $67,433 intraday after more than 140,000 BTC moved to a new wallet. It later recovered above $70,000 within days.

Read more: Bitcoin Enters Weak Seasonal Stretch As June Catalyst Test Nears