The measure passed as part of a housing bill. We break down what the US CBDC ban means for the crypto market and how other countries are approaching the issue.

The Senate passed the 21st Century ROAD to Housing Act by a sweeping 85-5 vote. The bill includes a temporary ban on the Federal Reserve issuing a central bank digital currency until December 31, 2030.

The bill now heads to the House, where swift passage is expected. It would then go to President Donald Trump for signature and take effect immediately. If Congress doesn’t extend the ban in 2030, the Fed would be barred from launching a CBDC without explicit legislative approval.

Contents

What the CBDC Ban Changes for the Fed and Stablecoins

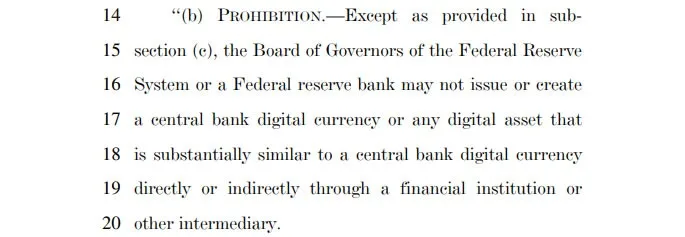

The bill says the Fed cannot directly or indirectly “issue or create a central bank digital currency or any digital asset substantially similar to a CBDC.” The restriction runs through the end of 2030.

A key exception is made for private stablecoins. The law explicitly allows “open, permissionless, and confidential dollar-denominated assets” that provide a level of privacy comparable to cash.

Adding the anti-CBDC provision to a housing bill is unusual but not uncommon–non-core measures are often attached to must-pass legislation to ensure support. Republicans, who have long pushed for such a ban, used the housing package as a political vehicle.

The Trump administration has consistently opposed CBDCs. In May, Treasury Secretary Scott Bessent confirmed the digital dollar is “off the table” and that the government will focus on passing the CLARITY Act crypto regulation bill.

Read more: The US Will Never Have Its Own CBDC — And Here’s Why

South Korea Testing CBDC in a Real Banking System

The rest of the world isn’t slowing down. On June 16, Reuters reported that China added 26 financial institutions to its digital yuan cross-border platform.

Meanwhile, the Bank of Korea is moving its CBDC pilot to the next phase. Nine commercial banks will create digital wallets, vouchers, and blockchain infrastructure to integrate digital money into the existing banking system. Earlier tests were limited to isolated payments through deposit tokens. Now, participants can use CBDC for real transactions and settlements.

The plan also includes replacing government subsidies and targeted payments with digital vouchers to boost efficiency and cut administrative costs.

The Atlantic Council’s latest tally shows three countries have already launched CBDCs, 41 are running pilots, 33 are in development, and another 40 are still researching.

Learn more: How to Pay with Stablecoins — Complete Guide for 2026