This review targets PSP founders, fintech squads, SaaS builders, online marketplaces, ISOs, and U.S. sellers wanting their own payment backbone. Sometimes “white label payment gateway” points to just a base system, sometimes it’s a coordination hub, an integrated payments suite, or a resale dashboard. The breakdown of white-label payment gateways here splits these options apart since picking one leans heavily on licensing range, transaction load, bank partner access, how risks are managed, plus what kind of seller is involved.

By June 2026, updates will shift how we check security proofs alongside API access levels. Instead of listing features one by one, think about path choices during transactions. Reporting on completed payments gets clearer when the structure improves behind the scenes. Pricing details? They tend to show up as quotes inside white-label gateway deals.

This piece could include links to partners. The order comes from a strict method, never payouts, balancing things like cost clarity, rules followed, match with needs, and safety checks.

Related: Best White Label Crypto Exchange Platforms for US Businesses In 2026

Contents

- 1.How To Compare A White Label Payment Gateway Solution

- 2.White-Label Payment Gateway Providers Reviewed in 2026

- 3.White Label Crypto Payment Gateway Use Cases

- 4.Decision Matrix For Payment Gateway White-Label Buyers

- 5.White-Label Payment Gateway Software Risks We Recommend to Avoid

- 6.Final Recommendation

How To Compare A White Label Payment Gateway Solution

Do not compare vendors by price alone. A white-label payment gateway must match the buyer’s jurisdiction, payment role, compliance scope, and transaction model.

Use this checklist:

- Licensing: confirm whether the vendor supports gateway, PSP, PayFac, ISO, or orchestration use cases.

- PCI DSS: request current security documents, tokenization scope, and card-data handling details.

- Routing And Settlement: check routing rules, cascading, settlement timing, reconciliation, and failed-payment logic.

- API and Reporting: test API docs, sandbox, merchant reports, exports, dashboard access, and role permissions.

- SLA and Cost: compare setup fee, monthly fee, transaction fee, support SLA, customization, and hidden add-ons.

Implementation risks:

- Vendor sales claims may not match sandbox performance.

- Compliance duties may shift if the buyer acts as PSP, PayFac, or merchant of record.

Expert Commentary: A compliance specialist should review the licence scope, PCI proof, data terms, and settlement responsibilities before contract approval.

Security, Compliance, And U.S. Payment Rules

One thing to note: safety isn’t everything. Look at how the provider handles laws, where payments go, when money lands, how smooth the tech links are, what reports show, response times for help, rule-following duties, and full pricing. Picking a vendor just because it’s cheap misses the point. Rules must matter just as much as features. What good is speed if risk piles up behind the scenes?

Use these five points before shortlisting a vendor:

Who handles the money flow might surprise you – it could be a gateway, maybe a processor. Sometimes it is the PayFac taking charge. Other times, an ISO works behind the scenes. The role shifts based on structure. One fits as an orchestrator, guiding transactions quietly. Licensing ties into who signs agreements. Payments depend on which hat they wear that day. Not always obvious at first glance.

1. Start by reviewing PCI DSS validation records before moving to how tokens replace real card details. Where payment info lives matters – check each storage point carefully. Look into business verification steps next, not skipping how disputes travel through systems. End with how long data stays, not just where it sits.

2. Start by looking at how payments move through the system. Check the paths they follow based on current guidelines. Timing matters when money finally lands in accounts – go over those windows carefully. Files that match incoming and outgoing records need close attention. When things do not go through, make sure there is clear oversight of what happens next.

3. Play around with a test sandbox before going live. Dive into clear guides that walk through every API function step by step. Dashboards show data in ways that make sense at a glance. Pull reports in formats your team already uses. Permissions change based on who needs what, nothing more.

4. Start with how often systems stay online when weighing service promises against price tags. Look at how fast help arrives after a request shows up on their end. Setup costs kick things off before anything runs live. Monthly payments keep access active over time. Each sale processed pulls a small cut from the total. Special changes to fit unique needs add extra line items. Fees stack differently depending on usage patterns.

5. Looking at different sellers means checking more than just what they promote. Instead of trusting brochures, dig into their rules for staying compliant, how tech works behind the scenes, feedback from others who used them, real examples of rollouts, plus fine print in contracts. What you need often shifts – location matters, business type counts, even duties a company handles make a difference.

It often happens that companies don’t grasp how strict U.S. rules really are. Sometimes a supplier sounds good when pitching, yet stumbles once tests begin – especially around trial runs, data sharing, or closing deals.

Hold off on paying setup costs until someone who knows regulations checks the vendor’s PCI DSS files, how they verify businesses, their method for handling conflicts, who owns the data, and what local laws apply. Rules around compliance, licenses, and daily operations can shift based on location and whether the provider acts as a processor or another type of party.

Routing, Settlement, And Merchant Controls

After things go live, the buyer’s hands-on control comes down to routing, settling payments, matching records, getting into the merchant dashboard, setting up sub-sellers, applying layered rules, and managing fees.

Don’t mix these tasks up with owning the acquisition piece or holding the ledger. Even if a gateway handles moving and directing payments, the bank that acquires still shapes whether approvals happen, when money lands, plus how fast everything starts running.

Getting started hinges on a sign-off from the acquiring partner, along with how smoothly backend systems connect. Business verification steps need to be cleared first. Only then does live deployment follow after final tech validations wrap up.

Related: Best Ways to Accept Crypto Payments for Businesses 2026

White-Label Payment Gateway Providers Reviewed in 2026

Down near the bottom, one option suits small teams better due to a simpler setup – though it lacks some reporting tools. Midway up, another stands out for strong uptime but hides extra fees in later billing cycles. Closer to the top, a pick built for fast scaling works well unless you handle cross-border payouts often.

Farther down, integration depth improves, yet onboarding takes longer than average. Near the peak, transparent pricing appears alongside strict contract terms that limit flexibility. Each tier shifts based on whether you run software services, process high volume, or manage global stores. This snapshot reflects comparisons made during June of 2026. No single score fits every business type – needs change if you’re embedded finance, a reseller, or a large retailer.

| Rank | Provider | Best Client Type | Platform Model | Strong Side | Main Limitation | Pricing Visibility | Data Status |

|---|---|---|---|---|---|---|---|

| 1 | Stripe | SaaS platforms, marketplaces, embedded payment products | Embedded payments, Checkout, APIs, Connect | Strong API documentation, hosted checkout, broad payment method coverage | Not a full white-label PSP core; branding and backend control have limits | Public pricing plus custom enterprise quotes | Verified from official docs and pricing pages |

| 2 | SDK.finance | PSPs, fintech startups, wallet products, payment businesses | White-label fintech and PSP software with source-code access | More control over product logic, merchant tools, and core payment workflows | Requires stronger internal technical, compliance, and product ownership | Public SaaS pricing plus custom enterprise options | Verified from official product and pricing pages |

| 3 | Akurateco | PSPs, payment resellers, merchants needing routing | White-label gateway and orchestration software | Routing, cascading, merchant tools, and PCI DSS-related positioning | Quote-based pricing; implementation scope must be checked before contract | Quote-based | Claimed by provider; key claims checked against public pages |

| 4 | Decta | Financial institutions, PSPs, acquirers, enterprise merchants | Gateway with acquiring and payment services angle | Combines gateway positioning with acquiring-related services and multi-currency support | Regional fit, onboarding terms, and vendor dependency require review | Not publicly listed; provider describes setup and recurring fees | Claimed by provider; public claims reviewed |

| 5 | Corefy | Payment institutions, high-volume merchants, routing-heavy teams | Payment orchestration platform | Routing, cascading, provider management, dashboard, and payment hub structure | Not a full PSP core or ledger replacement; external accounting may be needed | Not publicly listed on official site | Verified from official product pages; pricing requires vendor quote |

| 6 | NMI | ISOs, PayFacs, SaaS platforms, merchant service providers | White-label payment gateway backend | Partner-oriented gateway, merchant portal options, APIs, and broad payment acceptance | Feature access and commercial terms depend on partner agreement | Not publicly listed; partner-based pricing | Verified from official gateway pages |

| 7 | Spreedly | Enterprise merchants, SaaS, travel, marketplaces using several PSPs | Payment orchestration and vault layer | PSP abstraction, routing, vault, reporting, and gateway flexibility | Not a gateway core; performance depends on connected providers and contracts | Quote-based or not publicly listed | Verified from official product pages |

Stripe As a White-Label Online Payment Gateway Option

White label setups? Stripe handles those for embedded payments, no problem. Yet calling it a complete PSP replacement stretches things too far. Hidden boundaries show up under pressure. Built-in controls keep it from running wild. So yes, it fits certain roles neatly – just not every backend job. Limits shape where it works best.

Hosted checkout lives inside Stripe Payments. Think platforms, think marketplaces. Connect handles complex flows behind SaaS billing. Real-world usage spreads across different models. Cases pile up where systems must talk securely. One fits when money moves between parties at scale.

Includes APIs alongside branded checkout features. Payment links show up here, too. Fraud detection tools are part of it. Payouts get handled through the system. Over 125 payment types work within, ranging widely in origin and function.

Here’s the catch – Stripe runs the show behind the scenes. That means you cannot claim full control over how it looks or what happens under the hood. Ownership stays limited because the engine beneath belongs to them, not you.

| Parameter | Stripe Review | PROS | CONS |

|---|---|---|---|

| Main Product | Stripe Payments | Mature global payment infrastructure; Extensive documentation and developer tools | Core processing remains under Stripe control; Dependence on Stripe’s operational policies |

| Platform Tool | Stripe Connect | Strong support for marketplaces and platforms; Built-in onboarding and payout management | Platform logic must follow Stripe ecosystem rules; Some advanced workflows require custom development |

| Checkout Type | Hosted checkout and embedded checkout | Fast implementation with optimized payment flows; Conversion-focused user experience | Limited flexibility compared to fully custom checkout; Hosted elements reduce full UI control |

| Payment Methods | 125+ methods claimed | Broad payment method coverage across regions; Supports local and alternative payment methods | Availability varies by country and account setup; Some methods require additional compliance steps |

| Best For | SaaS, marketplaces, platforms | Well suited for recurring billing and platform payments; Scales effectively for growing digital businesses | Less suitable for highly customized PSP models; May not fit businesses needing full infrastructure ownership |

| PSP Core Fit | Limited | Can support many payment operations through APIs; Reduces need to build payment functionality from scratch | Not a complete PSP core platform; Limited control over underlying payment infrastructure |

| Branding Control | Partial | Allows some frontend customization; Supports branded payment experiences to a degree | Backend and infrastructure are not fully white-label; Stripe branding may remain visible in some flows |

| Pricing Visibility | Public pricing plus custom quotes | Easy to estimate standard costs; Transparent pricing for common services | Enterprise pricing may require direct negotiation; Additional fees can vary by product and region |

| Data Status | Verified from official docs and pricing pages | Information can be validated through public sources; Documentation is regularly maintained | Final capabilities depend on account type and contract terms; Features and availability may change over time |

SDK Finance White-Label Payment Gateway

Behind every smooth transaction, there sits software built for flexibility. One firm offers tools that let payment service providers run systems under their own brand. Think fintech startups, digital wallet teams, or any business moving money at scale. These groups often want deeper access than standard checkout pages allow. The platform steps in where off-the-shelf solutions fall short. Though it supports ready-made setups, full power comes from taking charge internally. That means handling code adjustments, legal checks, and system links in-house.

Ownership shifts from vendor to user when real control matters most.

When it comes to support, those using SaaS get updates handled for them. On the flip side, people working with source code must rely more on their own tech teams to keep things running smoothly.

Paying through the system means working with payment service providers, stores that accept payments, tracking records of money moving in and out, business-facing features for handling transactions, and linking up outside companies that handle payments. Tools built into the platform connect each part, so transfers run without delays or confusion across different services involved.

Out in the open, deployment might live in the cloud. Sometimes it slips into a SaaS setup instead. Other times, it runs straight from the source code. What shape it takes depends on how big the job is. The deal signed also plays a part.

| Parameter | SDK.finance Review | PROS | CONS |

|---|---|---|---|

| Main Model | White-label PSP and fintech platform | • Gives more product control than a simple hosted checkout• Supports customization of payment workflows and business logic | • Not a ready-made acquiring or processing solution• Requires additional integrations with payment providers |

| Best For | PSPs, wallets, fintech products | • Fits teams building payment products, not only accepting payments• Suitable for scalable fintech and PSP operations | • May be too complex for small merchants• Requires operational and technical resources |

| Source Code | Available through enterprise licence | • Can reduce long-term vendor dependency• Enables deep platform customization | • Requires in-house engineering ownership• Increases responsibility for maintenance and updates |

| SaaS Option | Available | • Faster to start than source-code deployment• Managed updates reduce operational workload | • Less control than a full source-code setup• Customization options may be more limited |

| Compliance Claims | PCI DSS Level 1 and ISO 27001:2022 claimed | • Helps reduce vendor due-diligence gaps• Supports enterprise compliance requirements | • Claims still need document review before contract• Compliance obligations remain with the business using the platform |

| Payment Role | Software platform, not acquiring bank | • Clearer separation between software and payment rails• Flexibility to choose acquiring and processing partners | • Buyer still needs acquiring and legal coverage• Additional vendor relationships may be required |

| Integration Need | High for source-code model | • Allows custom integrations and workflows• Supports tailored payment ecosystems | • Implementation can take longer than expected• Requires technical expertise and project management |

| Pricing Visibility | SaaS pricing public; enterprise/source-code quote-based | • Public SaaS pricing helps early budgeting• Easier initial cost estimation for SaaS deployments | • Enterprise cost is not fully visible before sales contact• Total implementation costs may vary significantly |

| Data Status | Verified from official pages | • Public claims can be checked during RFP• Information is available from official vendor sources | • Final terms depend on contract and deployment model• Public information may not reflect custom enterprise agreements |

Akurateco White-Label Payment Gateway Software For Routing

Built for fintech firms, payment service providers, and sellers, Akurateco offers a customizable payment system that handles routing and transaction oversight. Instead of building tech from the ground up, companies set up their own labeled environment using existing architecture. Tools inside manage how payments flow across providers while keeping control centralized. Admin features help track activity, adjust settings, and maintain operations – all under one roof. Each function works behind the brand’s name, giving a full ownership feel without heavy development.

Related: Top 10 Crypto Wallets (May 2026): Hot & Cold Options Reviewed

Starting off, the system handles transaction paths by linking different processors together – this keeps payments moving even if one provider fails. Instead of relying on just a single gateway, it spreads activity where needed. On top of that, businesses get access to controls for managing their setup, along with summaries of activity through visual displays. Reports come built-in, showing what happened when. Pages used during checkout can be adjusted to match specific needs, fitting into existing styles without forcing change.

Most people miss this: Akurateco builds tools but does not handle money directly. Processing payments only works through outside partners it links with. Before setting things up, businesses need to check what systems fit their setup. Details like rules, fees, and how changes can be made matter too.

| Parameter | Akurateco Review | PROS | CONS |

|---|---|---|---|

| Main Model | White-label gateway and payment orchestration platform | • Combines gateway and orchestration functions• Fits PSP and reseller infrastructure models | • Not an acquiring bank or settlement provider• Payment rails still depend on external partners |

| Routing | Routing, cascading, and provider selection | • Helps manage traffic across several providers• Can improve fallback logic when one route fails | • Routing quality depends on connected providers• Rules need testing with real transaction data |

| Orchestration | Multi-provider orchestration layer | • Useful for merchants or PSPs using several payment providers• Reduces dependence on one processor | • Does not replace processor contracts• Reconciliation can still require external accounting tools |

| PCI DSS | PCI DSS-certified claim by provider | • Gives buyers a document to request during due diligence• Can reduce card-data security gaps | • Certificate scope must be checked before contract• Buyer still has its own compliance obligations |

| Deployment Options | White-label setup with brandable payment pages and tools | • Allows branded payment experience• Faster than building a gateway from scratch in many cases | • Zero development cost should not be assumed without scope review• Custom workflows may still require technical work |

| Merchant Tools | Merchant management, reports, payment pages, and dashboards | • Supports merchant portfolio operations• Gives teams more control over daily payment activity | • Portal depth should be tested in sandbox• Feature access may depend on plan or agreement |

| Reseller Fit | PSPs, fintechs, payment resellers, and branded gateway providers | • Can support a reseller-style business model• Helps package payment services under one brand | • Commercial terms need direct review• Reseller duties may trigger legal and compliance checks |

| Pricing Visibility | Quote-based pricing | • Sales quote can reflect business size and transaction scope• Flexible pricing may fit complex PSP models | • Public cost comparison is limited• Setup, support, and customization fees must be clarified |

| Data Status | Public claims reviewed from official pages | • PCI DSS, routing, and provider claims can be checked during RFP• Official FAQ clarifies software-provider role | • Final capabilities depend on contract and integrations• Public claims may not reflect custom enterprise terms |

Decta As A White Label Payment Gateway Solution

Pulling Decta into play makes sense if you’re handling payments where acquisition, networks, disbursements, and gateways overlap tightly. A ready-made gateway setup could work well for fintechs dealing internationally. Cards involve processing options, onboarding support, pricing across currencies, and a go-live tied to risk approval. One strength stands out – combining merchant acceptance with infrastructure access, along with compliance-built paths. On the flip side, clear cost details are hard to find; assertions about performance require backing data.

| Parameter | Decta Review |

|---|---|

| Positioning | Branded cloud payment gateway |

| Best For | PSPs, acquirers, fintechs |

| Acquiring Coverage | Acquiring-related services available |

| Payment Methods | 100+ methods claimed |

| Supported Currencies | 150+ currencies claimed |

| Pricing Model | Setup cost plus recurring maintenance fee |

| Settlement Role | Depends on contract and acquiring setup |

| Vendor Lock-In Risk | Possible if integrations stay Decta-centered |

| Data Status | Public claims reviewed in June 2026 |

PROS: acquiring angle; broad currency coverage.

CONS: pricing is not fully public; migration terms need review.

Corefy As a White-Label Payment Gateway Platform

Most folks see Corefy as a payment switchboard, quietly linking systems behind the scenes. Instead of acting like a bank or handling money directly, it lines up tools that manage transactions. Picture wires connecting processors, gateways, and reporting screens into one view. Routing paths shift based on rules, failures, or performance hiccups. Merchants tweak settings through their own labeled interface – no code needed. Think of it less as financial infrastructure, more as command center software. Not where payments land, but how they get directed. Ownership stays clear. Decisions happen fast. Oversight remains local.

Start by linking current PSPs, then bring in acquirers alongside available payment methods using Corefy’s routing backbone. One step ties them together under a single flow. Each piece plugs into the system without replacing what already works. The structure holds everything in sync behind one interface. No overhaul needed just to add new options. Everything talks through a shared middle layer. Integration runs quietly beneath daily operations.

Start by setting up how data moves through the system. Then comes linking connected features, so changes flow naturally. Dashboards appear next, shaped around user needs. Access to the merchant portal follows its own path, controlled step by step. Compliance settings wrap it up, built into each layer along the way.

Should outside tools handle bookkeeping, map those steps early. When company processes need oversight, line up tracking methods ahead of time. If payment records rely on outside systems, set rules now. Finance tasks that depend on third parties? Arrange checks before rolling out. Internal work might demand external controls – build them in from the start.

| Parameter | Corefy Review | PROS | CONS |

|---|---|---|---|

| Main Model | White-label payment orchestration platform | • Supports branded payment operations• Combines provider control and merchant-facing tools | • Not a full PSP core• Does not replace acquiring or processing contracts |

| Provider Connections | 600+ provider connections claimed | • Gives access to broad payment coverage• Helps expand methods without building every integration | • Public claim still needs RFP verification• Availability depends on provider contracts |

| Routing | Smart routing and cascading tools | • Helps distribute traffic across providers• Can support fallback when one route fails | • Routing rules need testing before launch• Results depend on processor performance |

| Dashboard | Central interface for payment operations | • Helps monitor transactions in one place• Useful for multi-provider management | • Dashboard depth should be checked in demo• Custom reports may need extra setup |

| Merchant Portal | Branded merchant-facing tools | • Supports white-label merchant operations• Can simplify merchant portfolio management | • Portal scope may depend on agreement• Not the same as owning backend infrastructure |

| Compliance Controls | Compliance-readiness and card-program participation claimed | • Gives buyers documents to request during due diligence• Supports structured payment operations | • No legal guarantee for buyer compliance• PCI, KYB, and data terms still need review |

| Settlement Logic | Works above connected providers | • Can centralize payment visibility• Helps compare provider performance | • Settlement depends on acquirers and PSPs• Accounting logic may require external systems |

| Pricing Visibility | Not publicly listed | • Quote can reflect volume and integration scope• Flexible for complex payment setups | • Harder to compare total cost early• Setup, support, and customization fees need clarification |

| Data Status | Public claims reviewed in June 2026 | • Official pages confirm orchestration positioning• Claims can be checked during RFP | • Final terms depend on contract• Public pages do not replace technical discovery |

NMI Payment Gateway White Label Solution For ISOs

White-label payments come alive through NMI, built for ISOs, PayFacs, or software firms wanting their own name on checkout flows. Branding sits up front, yet teams rely on NMI beneath the surface for transaction handling. Merchant dashboards, sign-up steps, help systems show up ready-made – API keys open doors too. But control stops short of approval logic, bank relationships, money movement, or risk decisions. It fits best if you’re set on guiding stores under your logo while riding NMI’s network behind the scenes.

Access varies by location, so confirm where it works first. Not every processor links here; partnerships hinge on current deals struck. Hidden rules might shape what resellers can do – get clarity directly from NMI before agreements. Surprises fade once real talk happens about program fine print ahead of commitment. Tech runs deep, though freedom has limits baked into the model from the start.

Depending on where you are, what channel runs things might shift. A given processor could change which tools show up. Commercial deals also play a role in what gets unlocked. Think of it more like connecting pieces through partners. It does not act as an entire payment operation ready to go. Not every region sees the same setup appear.

| Parameter | NMI Review | PROS | CONS |

|---|---|---|---|

| Best Fit | ISOs, PayFacs, SaaS platforms, and merchant service providers | • Fits partner-led merchant portfolios• Useful for embedded payment monetization | • Too complex for simple merchants• Partner approval may be required |

| Branding | White-label gateway and branded merchant experience | • Helps partners present payment tools under their brand• Supports merchant-facing consistency | • Branding does not mean full backend ownership• Some NMI or processor dependencies may remain |

| Merchant Support Portal | Merchant and partner portal access available | • Helps manage merchants and transactions• Supports portfolio-level operations | • Portal depth should be tested before contract• Feature access may depend on agreement |

| Onboarding | Merchant onboarding and relationship tools | • Can support merchant acquisition workflows• Useful for ISOs managing many accounts | • Underwriting still depends on payment partners• Regional rules can affect onboarding speed |

| APIs | Gateway APIs and integration tools | • Supports ecommerce, in-person, and embedded flows• Helps SaaS teams connect payment functions | • API work still needs developer resources• Custom use cases may need extra review |

| Backend Role | Gateway infrastructure provider | • Reduces need to build gateway backend internally• Gives access to established gateway rails | • Does not guarantee full control over processing• Settlement terms depend on provider setup |

| Processor Connections | 150+ global processor connections claimed | • Broad processor choice can reduce lock-in• Useful for multi-market payment strategies | • Not every processor is available everywhere• Contract terms vary by partner and region |

| Pricing Visibility | Not publicly listed; partner-based pricing | • Pricing can reflect business model and volume• Better fit for ISO or SaaS partner structures | • Harder to compare early costs• Support, setup, and extras need clarification |

| Data Status | Public claims reviewed in June 2026 | • Official pages support gateway and ISO positioning• Portal and connection claims are checkable | • Final availability depends on contract• Public pages do not replace partner due diligence |

Spreedly White-Label Payment Gateway Software For Orchestration

Not built as a gateway at its base, Spreedly connects systems across multiple processors. Companies using many gateways find it useful, as well as those managing separate fraud tools or local payment types. When storage of card data matters, along with smart transaction paths and oversight reports, the platform fits well. Full control over branding isn’t always needed; sometimes coordination beats total ownership. Shifting between providers becomes easier, especially while keeping old contracts alive.

Trying out new processing lanes? That gets simpler, too. Locked-in risk drops because switching doesn’t demand checkout rewrites. Stored details move smoothly from one system to another. Yet tracking exact costs can get tricky. Success still leans heavily on whatever external providers stay linked. What a system can do often ties back to its processor type, agreed terms, where it operates, and how payments are handled. Last verification happened through confirmed sources in mid-2026 as part of standard supplier checks.

| Parameter | Spreedly Review | PROS | CONS |

|---|---|---|---|

| Main Model | Open payments connectivity and orchestration layer | • Reduces dependence on one provider• Fits multi-PSP payment teams | • Not a white-label gateway core• Still depends on connected processors |

| Vault | Secure payment-method vault and tokenization layer | • Helps abstract stored payment methods• Supports future provider migration | • Vault scope must be checked contractually• Token portability can depend on setup |

| Routing | Routing across connected gateways and processors | • Useful for fallback and optimization• Helps test provider performance | • Routing quality depends on PSP response• Rules need operational monitoring |

| Fraud Tools | Fraud and authentication orchestration through Protect | • Can combine fraud checks with authorization• Supports 3DS-related workflows | • Fraud coverage depends on enabled tools• Extra services may affect total cost |

| Reporting | Central payment visibility across providers | • Helps compare processor performance• Useful for multi-provider operations | • Reporting depth should be tested• Finance exports may need extra work |

| Vendor Abstraction | Layer between merchant and PSPs | • Helps reduce processor lock-in• Supports more flexible payment strategy | • Does not remove PSP contracts• Provider terms still control availability |

| Best Use Case | Enterprise merchants, SaaS, travel, marketplaces | • Strong fit for complex payment stacks• Better than core when existing PSPs stay | • Less suitable for launching PSP infrastructure• Not enough alone for acquiring operations |

| Pricing Visibility | Quote-based or not publicly listed | • Pricing can reflect scale and complexity• May fit enterprise payment models | • Hard to compare early costs• Add-ons can change final price |

| Data Status | Public claims reviewed in June 2026 | • Official pages confirm orchestration positioning• Features can be checked during RFP | • Public pages do not replace technical discovery• Final scope depends on contract |

White Label Crypto Payment Gateway Use Cases

When speed matters across borders, stablecoins help merchants move money quickly – linking suppliers, regional partners, or distant teams without delay. Regions connect more smoothly when payments clear fast, especially where banking lags. Remote groups gain rhythm when funds arrive predictably, tied to real-world value. Timing tightens when settlements skip traditional queues. Value holds steady when volatility stays out of the equation.

Read more: Why Solana Is Dominating Crypto Payments in 2026

For fintech tools, trading platforms, games, digital items – places where people keep cryptocurrency – a wallet-based payment flow fits naturally. Where crypto lives, spending it straight from storage makes sense. Think of apps tracking money moves, markets swapping tokens, and virtual worlds selling assets. Users already there do not need extra steps. Their funds sit ready inside personal wallets. Moving value becomes direct when the system speaks the same language. No bridges required. Built-in access lowers friction without inviting trouble. This approach lines up with how these spaces operate today.

Check three risks before launch:

1. When store owners hide who they really are, risk grows. Data gaps pop up if the Travel Rule details vanish somewhere along the way.

2. When prices swing fast, risk shows up in different ways. One moment, it hides in wild token shifts. Then suddenly appears through thin stablecoin pools. Sometimes waits quietly till cashing out gets slow. Each delay adds another layer of exposure.

3. Money might vanish if a wallet gets locked. Some regions could limit access entirely.

Hold off on turning things live without a money expert checking how assets are held, swapped, cleared, and reported. Remember, this isn’t guidance you can rely on legally or financially.

Crypto Gateway Architecture For White Label Teams

Out of the gate, a customer pays using cryptocurrency. Following that transaction, funds move into secure wallet storage managed by custodians. Then comes compatibility with stablecoins – making value transfers more predictable. Afterward, every movement gets tracked across the blockchain in real time. Checks against money-laundering rules happen next, quietly running in the background. Once cleared, digital assets turn into regular currency through conversion. Finally, a full summary wraps up the entire flow at journey’s end.

A wallet forms just a single piece in a white-label crypto payment system. Even so, systems require clear protocols around holding funds, tracking transactions, turning crypto into local currency, handling returns, and record-keeping. When custody is managed by the service or its authorized agent, they hold the access codes. If it’s non-custody based, those keys stay with the business or customer – yet oversight and regulatory steps remain necessary. Building such a solution demands a distinct legal evaluation before going live.

Operational risks:

Delayed confirmations can break order status;

Poor reconciliation can create accounting gaps.

Fees, Risk, And White Label Payment Gateway Price

Pricing for a white-label payment gateway shifts based on how it’s built, access each month, how many transactions flow through, security rules, custom features, and what kind of help is promised. When monthly volume hits $100,000, just a 0.20% cut means spending $200 – this comes before extra charges pile up. Quotes often hide details; that’s why an RFP must ask for every single cost listed out..

| Cost Item | Pricing Status | Example For $100,000 | Hidden Fee Area | Risk | Check Before Contract |

|---|---|---|---|---|---|

| Setup fee | quote-based | upfront | onboarding | budget overrun | implementation scope |

| Monthly fee | range/quote | fixed | minimums | margin loss | included modules |

| Transaction fee | %/quote | $200 at 0.20% | volume tiers | higher blended cost | effective rate |

| PCI fee | quote/status | varies | audit help | compliance gap | PCI scope |

| Customization fee | quote-based | project-based | API changes | delays | statement of work |

| Support SLA | quote-based | monthly/add-on | priority support | slow incidents | response time |

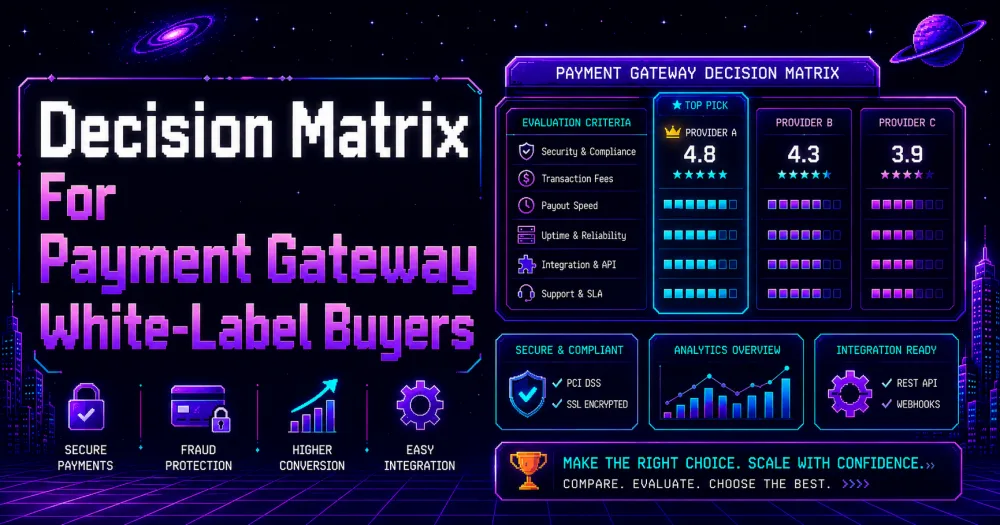

Decision Matrix For Payment Gateway White-Label Buyers

Depending on your business size, the volume of transactions you handle, what licences you hold, access to acquirers, and how much engineering talent sits inside your team, your ideal white-label payment gateway shifts. That matrix for filtering gateways? It trims down options just fine, yet still leaves room for RFPs, legal checks, plus deep tech exploration.

Start here instead of features – business models show how companies actually work. Look at who makes money how, before checking boxes on a list. One size never fits all when survival depends on different paths.

| Scenario | Preferred Model | Key Risk | Cut-Off Criterion |

|---|---|---|---|

| PSP Launch | White-label gateway core | Compliance scope and acquiring readiness | No PCI proof or merchant onboarding workflow |

| SaaS Monetization | Embedded payments platform | Limited backend control | No split payments or platform reporting |

| Marketplace | PayFac-style or platform payments | Seller KYB and payout risk | No sub-merchant management |

| Bank | Vendor core with audit controls | Procurement, data, and risk ownership | No audit documents or data terms |

| Crypto Settlement | Crypto gateway layer | AML, sanctions, volatility | No wallet screening or Travel Rule process |

| Enterprise Fallback | Orchestration layer | Processor dependency | No routing sandbox or reconciliation export |

🔶 Expert Commentary: Compare vendors by business model first, not by feature count alone.

White-Label Payment Gateway Software Risks We Recommend to Avoid

Just because warning signs show up does not automatically make a provider risky. It simply means the white label payment gateway stays off the list – until contracts, costs, and system details get checked. What matters comes after proof.

No PCI Proof

Here’s why: proof of up-to-date PCI DSS coverage is missing. Security records aren’t available right now. That makes verification impossible. Without documents, there’s no way forward. The requirement remains unmet. Full stop.

Still foggy who handles card data tasks, when tokens apply, and who answers after a leak. Responsibility floats without clear lines drawn.

Before signing, share your PCI paperwork. Show how tokenization works step by step. Include rules for handling data. Give the latest version of access controls. What’s inside each document matters just as much as having them.

Unclear Fees

Hidden fees pop up in setup charges. Monthly billing adds unseen expenses. Transactions carry extra pricing layers. PCI compliance sneaks in added cost. Custom work means surprise invoices. Support agreements include undisclosed rates.

Here’s a twist – profits might vanish once the white-label payment system goes live.

Before signing anything, do you have a complete list of fees ready to share?

Weak Documentation Or No Sandbox

Missing pieces block progress. The API documentation has not been shared. Without a test setup, checking changes gets harder. A process for handling disputes does not exist yet. Export tools for matching records are also absent.

Unexpected hiccups in merging systems might slow things down. Getting merchants set up could hit a snag along the way.

Before signing, does your team allow us to try out the API? Testing reporting features ahead of time would help. Routing checks matter too – can we run through those? Dispute processes included in trial access? Payment comes later, after these pieces work.

Three Vendor Red Flags Before Signing

Use this RFP checklist before contract review:

Only when you sign does the full cost appear. Fees tucked away might shrink profits later. Check what it takes to start things up. Look at what comes each month. Review how much they take per sale. Confirm their security rules are clear. See exactly what changes will cost. Know how fast help arrives if systems fail.

RFP Question: What is the full fee schedule before signing?

Refunds might take longer if there’s a disagreement, while proof sharing and matching records happen later. Check how returns work, handle conflicts, then test exports – all inside the trial space.

RFP Question: How are chargebacks tracked, assigned, and exported?

Ownership gaps in records? That raises risk during transfer. Check the agreement details first – clarity on handling info matters just as much.

RFP Question: Who owns tokens, logs, merchant data, and exports?

Before putting pen to paper, someone must check the legal details. A signature needs clearance first.

Frequently Asked Questions on White Label Online Payment Options

What Is a White-Label Payment Gateway?

Ready-made payment systems can wear a company’s name on the surface. Unlike regular gateways, these include custom branding along with added control for sellers. Instead of full orchestration setups, they behave more like basic gateway tools. Ownership of what happens behind the scenes still leans on the provider – unless paperwork says different.

How Do White-Label Payment Gateway Prices Vary?

Pricing for a white-label payment gateway changes based on how it’s built, what you pay each month, how many transactions run through it, special features needed, rules it must follow, and service response promises. You won’t often find public rate sheets – instead, ask for a detailed proposal or official estimate. When there’s nothing listed online, go with quotes tailored to your case. Skip general numbers if nobody can back them up.

Can a White-Label Cryptocurrency Payment Gateway Support Stablecoins?

Stablecoins might work – though only if custody checks out, along with anti-money laundering reviews. Blockchain tracking needs to be active, plus a solid link to a settling bank and the right country rules. Offering a branded crypto gateway? Then forget hiding user identities or skipping identity checks. Trouble could come from price swings, missed sanction alerts, or even locked balances without warning.

Which Gateway Software Features Matter Most?

Start with the API documentation, then move to sandbox setup – linking routing and tokenization early helps spot gaps. Reporting ties into reconciliation through the merchant portal, while role-based access shapes user limits. Check every function in the test environment before examining contracts. Even full features won’t prevent hiccups if the SLA lacks clarity, incidents aren’t mapped out, or support duties stay undefined.

How Should A Payment Gateway White-Label Solution Be Compared?

Start by looking at suppliers using an RFP, then move to checking their security papers. A test environment helps see how things work before committing. Fees matter – model them out carefully instead of guessing. Review contracts line by line; never skip that step. Rankings limit understanding, so avoid turning options into a numbered list. What shapes the last call? Legal boundaries play a part. So does what the acquiring bank demands. Plans count just as much. Where the provider fits in the whole payment flow makes a difference, too.

Final Recommendation

Picking a full white-label core makes sense if you’re building something like a PSP, ISO, or PayFac setup where your brand runs the whole show – think custom onboarding, transaction paths, and how fees are set. When existing processor links are already in place, orchestration steps in to handle traffic flow, backup options, and match up records behind the scenes.

For software platforms or online markets aiming to generate revenue more quickly while skipping the management of complex back-end systems, embedded payments offer a lighter path forward. Stay away from providers who can’t prove PCI compliance, lack testing environments, or leave questions about who owns the data.

Using a rebranded payment gateway might seem clean at first, yet hidden costs appear easily, particularly when quotes replace clear pricing. Before sending any money, look over the agreement terms closely. A test run helps – ask for one along with responses to your RFP. Papers about the rebranded payment system should come too. Check what you’re signing up for fully.

Author and update note

This piece came together under the guidance of someone who spends days inside payment systems, sorting through how providers connect, welcome businesses, and handle gateways. Refreshed mid-June, two thousand twenty-six. Their role shapes the approach, sets what gets weighed, and verifies every detail.

Sources and Verification Links

Access date for all sources: 16 June 2026.

* https://stripe.com/resources/more/white-label-payment-gateways

Verified: general definition of a white-label payment gateway and comparison context.

* https://docs.stripe.com/payments/checkout

Verified: Stripe Checkout, hosted checkout, embedded checkout, and 125+ local payment methods.

* https://docs.stripe.com/connect

Verified: Stripe Connect use cases for SaaS platforms, marketplaces, and multi-party payments.

* https://stripe.com/payments/payment-methods

Verified: Stripe payment method coverage and 125+ payment methods claim.

* https://stripe.com/pricing

Verified: Stripe public pricing page and availability of custom pricing.

* https://stripe.com/pricing/local-payment-methods

Verified: local payment method fees and custom pricing note.

* https://docs.stripe.com/payment-links

Verified: Stripe Payment Links and hosted payment page functionality.

* https://docs.stripe.com/payments/elements

Verified: Stripe Elements and customizable checkout UI components.

* https://docs.stripe.com/radar

Verified: Stripe Radar fraud monitoring and transaction risk tools.

* https://sdk.finance/solutions/white-label-psp-solution/

Verified: SDK.finance white-label PSP positioning, source-code model, PCI DSS Level 1, and ISO 27001:2022 claims.

* https://sdk.finance/pricing-saas/

Verified: SDK.finance SaaS pricing availability.

* https://sdk.finance/pricing/

Verified: SDK.finance enterprise/source-code pricing model and quote-based enterprise scope.

* https://sdk.finance/getting-started/

Verified: SaaS and Source Code deployment models.

* https://sdk.finance/blog/top-white-label-payment-gateway-providers/

Used for competitor comparison context and white-label gateway market framing.

* https://akurateco.com/

Verified: Akurateco white-label payment software positioning, payment gateway role clarification, and software-provider status.

* https://akurateco.com/lp/white-label-payment-gateway.html

Verified: Akurateco PCI DSS-certified claim, 650+ integrated payment providers claim, branding, routing, and gateway software positioning.

* https://akurateco.com/faq

Verified: Akurateco does not participate in financial flow, processing commissions, or settlements.

* https://akurateco.com/blog/whats-a-payment-gateway-reseller-program

Verified: reseller-program context and payment gateway reseller model.

* https://akurateco.com/blog/how-does-payment-orchestration-work

Verified: routing, cascading, settlement, reconciliation, and payment orchestration logic.

* https://www.decta.com/products/white-label-payment-gateway

Verified: Decta cloud-based white-label gateway, branding, payment methods, omnichannel tools, and merchant management.

* https://www.decta.com/company/media/best-white-label-payment-gateway-providers

Verified: Decta comparison data, 100+ payment methods, 150+ currencies, and setup plus recurring monthly maintenance pricing model.

* https://www.decta.com/company/media/how-to-choose-a-white-label-payment-gateway-for-acquirers-2026-guide

Used for acquirer-focused comparison context and white-label gateway selection criteria.

* https://corefy.com/white-label-payment-gateway

Verified: Corefy white-label payment gateway positioning, 600+ provider connections, smart routing, cascading, dashboard, and provider-management claims.

* https://corefy.com/security-and-compliance

Verified: Corefy PCI DSS Level 1 environment and security/compliance positioning.

* https://corefy.com/build/media/files/Security%26Compliance.82a86cf1fb10ef9527b71e834fb039ce.pdf

Verified: Corefy Visa TPA, Mastercard Registration Program, PCI DSS, and security documentation claims.

* https://corefy.com/blog/best-white-label-payment-gateway-providers

Used for competitor comparison context and payment orchestration framing.

* https://www.nmi.com/

Verified: NMI white-label gateway positioning, ISOs, SaaS, 150+ processor connections, active merchants, channel partners, and embedded payments positioning.

* https://www.nmi.com/products/payment-gateway/

Verified: NMI payment gateway white-label solution and gateway feature positioning.

* https://www.nmi.com/who-we-serve/independent-sales-iso/

Verified: NMI ISO use case and partner-oriented payment gateway positioning.

* https://www.nmi.com/developers/sdks-apis/

Verified: NMI APIs, SDKs, developer tools, and integration resources.

* https://docs.nmi.com/

Verified: NMI developer documentation, sandbox-to-production process, and API documentation.

* https://docs.nmi.com/reference/getting-started

Verified: NMI API starting point, payment processing, secure storage, reporting, and integration scope.

* https://www.nmi.com/resources/payments-101/fundamentals/knowing-your-path-iso-payfac-or-software-developer/

Verified: difference between ISO, PayFac, and software developer roles, including risk and compliance responsibility.

* https://www.spreedly.com/

Verified: Spreedly open payments platform, reporting, reconciliation, fraud prevention, authentication, and orchestration positioning.

* https://www.spreedly.com/blog/open-payments-platforms

Verified: open payments platform definition and multi-provider integration logic.

* https://www.spreedly.com/blog/open-payments-and-fraud-prevention

Verified: Spreedly fraud-prevention integrations and provider-abstraction context.

* https://www.spreedly.com/blog/combat-online-payment-fraud

Verified: Spreedly Protect, fraud management, authentication, and 3DS-related orchestration.

* https://www.pcisecuritystandards.org/

Verified: PCI SSC official standards source.

* https://www.pcisecuritystandards.org/document_library/

Verified: PCI DSS v4.0.1 document library, PCI resources, SAQ, ROC, and official security documentation source.

* https://blog.pcisecuritystandards.org/just-published-pci-dss-v4-0-1

Verified: PCI DSS v4.0.1 publication and active standard context.

* https://www.fincen.gov/resources/statutes-regulations/guidance/application-fincens-regulations-certain-business-models

Verified: FinCEN CVC guidance page, MSB context, and applicability to virtual currency business models.

* https://www.fincen.gov/system/files/2019-05/FinCEN%20Guidance%20CVC%20FINAL%20508.pdf

Verified: FinCEN guidance on convertible virtual currency, money transmission, and MSB obligations.

* https://ofac.treasury.gov/recent-actions/20211015

Verified: OFAC virtual currency sanctions compliance guidance publication.

* https://ofac.treasury.gov/media/913571/download?inline=

Verified: sanctions compliance guidance for the virtual currency industry.

* https://ofac.treasury.gov/faqs/topic/1626

Verified: OFAC virtual currency FAQs, blocked property, reporting, and sanctions-related risks.

* https://www.fatf-gafi.org/en/topics/virtual-assets.html

Verified: FATF virtual assets definition and AML/CFT context.

* https://www.fatf-gafi.org/en/publications/Fatfrecommendations/Guidance-rba-virtual-assets-2021.html

Verified: FATF risk-based approach for virtual assets and VASPs.

* https://www.fatf-gafi.org/en/publications/Fatfrecommendations/targeted-update-virtual-assets-vasps-2024.html

Verified: FATF Recommendation 15 update context, AML/CFT measures, and VASP supervision.

* https://www.fatf-gafi.org/en/publications/Fatfrecommendations/update-Recommendation-16-payment-transparency-june-2025.html

Verified: FATF Travel Rule and payment transparency update.

* https://www.getivy.io/blog/best-white-label-payment-gateways

Used for competitor comparison context only; provider facts were checked against official sources.

* https://wise.com/gb/blog/white-label-payment-gateway

Used for competitor comparison context and buyer-side white-label gateway considerations.

* https://boxopay.com/blog/white-label-payment-gateway-guide-solutions-comparison/

Used for competitor comparison context only; claims were not treated as primary verification.